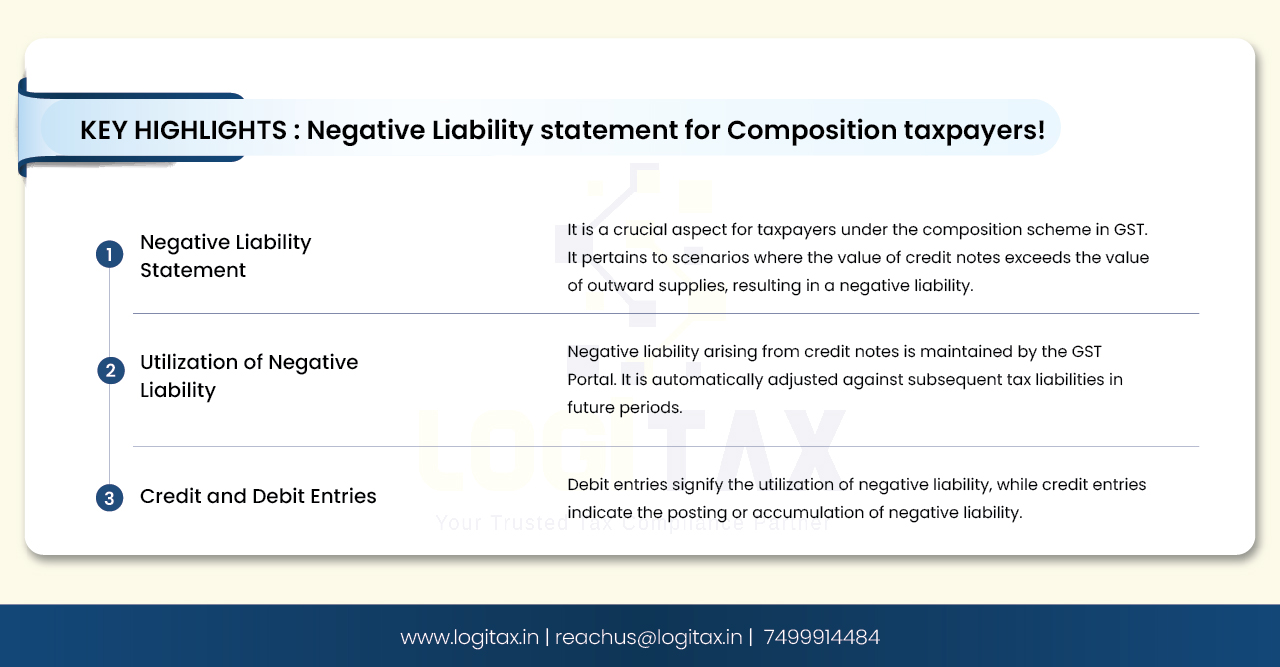

In the case of taxpayers who have opted for a composition scheme, they report the tax liability net of credit /debit notes. In some cases, the value of credit notes exceeds the value of outward supplies. In such cases, the liability becomes negative. In such a scenario, where the taxpayers have negative liability in Form GST CMP-08 or Form GSTR-4 (Annual), the same is posted to the Negative Liability Statement.

In case there is any negative liability in a tax period and no amount is payable during that tax period by the taxpayer, then such negative liability is maintained by the GST Portal in Negative Liability Statement. The Balance, if any, lying in the Negative Liability Statement, will automatically be adjusted against the liability of subsequent tax period(s). The Negative Liability Statement is only for view purposes by the taxpayers and cannot be edited.

For E.g.: If Tax Amount of Outward Supplies (CGST+SGST/IGST) = Rs 2,00,000 and Tax Amount of credit notes (CGST+SGST/IGST) issued = Rs 2,50,000, then negative liability = -50000

| Description | IGST | CGST | SGST | Total |

|---|---|---|---|---|

| Tax component on Outward supplies during a tax period say Q1 | 1,00,000 | 50,000 | 50,000 | 2,00,000 |

| Tax component of credit notes issued during the tax period Q1 | 1,00,000 | 70,000 | 70,000 | 2,50,000 |

| Negative Liability (available for utilization towards supplies in future tax periods) | -10,000 | -20,000 | -20,000 | -50,000 |

| Tax component on Outward supplies made during next tax period say Q2 | 10,000 | 15,000 | 15,000 | 40,000 |

| Tax amount adjusted against the Negative Liability | 10,000 | 15,000 | 15,000 | 40,000 |

| Negative Liability (available for utilization in future tax periods) say Q3 | 0 | -5,000 | -5,000 | -10,000 |

In the above example, Rs 50000 will be posted as a credit entry in the Negative Liability Statement.

In the next tax period if the total liability is Rs 40,000, then out of Rs 50,000, Rs 40,000 will be utilized. Then, there will be a debit entry posted in the Negative Liability Statement for Rs 40,000 and so on.

The meaning of Debit is that the amount is debited or utilised and the meaning of Credit is that the amount is credited or posted.

Yes, the Negative Liability Statement is maintained for both reverse charge and other than reverse charge liability separately via different columns for each.

In conclusion, the Negative Liability Statement for composition taxpayers under GST provides a mechanism to address situations where the value of credit notes exceeds the value of outward supplies, resulting in negative liability. This statement helps taxpayers track and manage their liabilities, with any negative balance automatically adjusted against subsequent tax periods. It offers transparency and accountability in tax reporting, ensuring compliance with GST regulations.

composition scheme under gst

gst composition scheme

composition scheme

composition scheme in gst

composition scheme gst

25-07-2024

GST

Mrudula Joshi

CBIC had issued Circular No. 227/21/2024-GST on 11th July, 2024. A revised procedure for Read More

24-07-2024

GST

Mrudula Joshi

In the recent budget announced on July 23, 2024, several key changes were made to the tax structure in India. Read More

23-07-2024

E-Invoice

Mrudula Joshi

The landscape of Goods and Services Tax (GST) compliance in India is continuously evolving, Read More

18-07-2024

GST

Mrudula Joshi

On June 22, 2024, the 53rd GST Council meeting was held in Delhi, with Union Minister for Read More

17-07-2024

GST

Mrudula Joshi

The Central Board of Indirect Taxes and Customs (CBIC) has issued a circular to clarify Read More

17-07-2024

GST

Mrudula Joshi

Notification No. 04/2024- Central Tax dated 05th January 2024, all the registered persons engaged in manufacturing Read More

15-07-2024

GST

Mrudula Joshi

On June 22, 2024, the 53rd GST Council meeting was held in Delhi, with Union Minister for Finance and Corporate Affairs, Read More

11-07-2024

GST

Mrudula Joshi

On June 22, 2024, the 53rd GST Council meeting was held in Delhi, with Union Minister for Finance and Corporate Affairs, Read More

09-07-2024

GST

Mrudula Joshi

To help the taxpayers make data entries faster and to reduce errors while creating their Statement of outward supplies in Form GSTR-1, Read More

08-07-2024

GST

Mrudula Joshi

STAK (Single time authentication key) which can be generated using the “GST SECURE OTP” mobile application that a Read More

06-07-2024

GST

Mrudula Joshi

A Digital Signature Certificate (DSC) is a secure digital key issued by government-authorized certifying authorities to verify the identity of the certificate Read More

05-07-2024

GST

Mrudula Joshi

For online signing of legally binding documents, emSigner is a dependable choice. This web-based platform allows Read More

03-07-2024

GST

Mrudula Joshi

On June 22, 2024, the 53rd GST Council meeting was held in Delhi, with Union Minister for Finance and Corporate Affairs Read More

01-07-2024

GST

Mrudula Joshi

On June 22, 2024, the 53rd GST Council meeting was held in Delhi, with Union Minister for Finance and Corporate Affairs, Read More

25-06-2024

GST

Mrudula Joshi

As per section 78 of the CGST Act, 2017, recovery proceedings under GST can be initiated after three months' expiry Read More

Products

Products